What Every Employer, Employment Agency and Migrant Worker Should Know

Foreign Worker Medical Insurance (FWMI) is a mandatory requirement for employers hiring Work Permit holders in Singapore. While every employer purchases this insurance, many are still unsure about what it actually covers.

Some common questions include:

- Does FWMI cover a worker’s visit to a GP for fever or flu?

- Will hospitalization bills be paid by the insurer?

- If I make a claim, will my insurance premium increase next year?

Let’s break it down in simple terms.

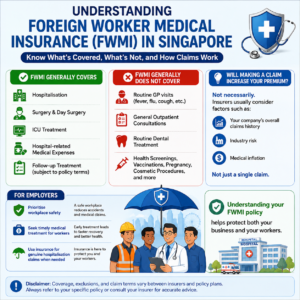

🏥 FWMI Is Primarily Hospitalisation Insurance

The main purpose of FWMI is to protect employers from unexpected and expensive medical bills when a worker requires hospital treatment.

Typical FWMI plans generally cover:

✅ Hospital ward charges

✅ Intensive Care Unit (ICU)

✅ Surgery and day surgery

✅ Operating theatre charges

✅ Anesthesia

✅ Medicines administered during hospitalisation

✅ Diagnostic tests conducted during admission

✅ Daily doctor’s visits while admitted

✅ Post-hospitalisation follow-up treatment (subject to policy conditions)

✅ Rehabilitation after hospitalisation (where applicable)

✅ Ambulance charges (subject to policy limits)

If a worker is admitted for conditions such as:

- Dengue fever

- Pneumonia

- Appendicitis

- Serious infections

- Bone fractures requiring surgery

the hospitalization expenses are generally covered according to the policy terms and benefit limits.

👨⚕️ Are Specialist Consultations Covered?

Yes—but only under specific circumstances.

Most FWMI plans cover specialist consultations when they are directly related to a condition that eventually requires:

- Hospital admission; or

- Day surgery.

Likewise, follow-up consultations after discharge are often covered for a limited period if they are related to the same medical condition.

Routine specialist consultations that do not lead to hospitalization are generally not covered.

❌ Does FWMI Cover Normal GP Visits?

This is probably the biggest misconception among employers and workers.

If a worker visits a clinic for:

- Fever

- Flu

- Cough

- Headache

- Sore throat

- Gastric pain

- Minor skin infections

👉 Generally, these visits are NOT covered under standard FWMI.

FWMI is primarily designed for hospitalization and surgical expenses, not everyday outpatient medical consultations.

Routine GP visits are usually borne by the employer unless a separate outpatient medical plan has been purchased.

🦷 What About Dental Treatment?

Most FWMI plans only provide coverage for accidental dental injuries.

Examples:

✅ Tooth damaged due to an accident

❌ Scaling and polishing

❌ Fillings

❌ Wisdom tooth extraction

❌ Dentures

❌ Dental implants

🌍 Overseas Medical Treatment

Emergency hospitalization while overseas may be covered under certain FWMI policies.

However, planned overseas medical treatment and routine overseas clinic visits are generally excluded.

🚫 What Is Usually Not Covered?

Although every insurer’s policy differs, common exclusions include:

- Routine health screening

- Vaccinations

- Pregnancy and childbirth

- Cosmetic procedures

- Traditional Chinese Medicine (TCM)

- Chiropractic treatment

- Routine physiotherapy (unless linked to a covered hospitalization)

- Weight loss treatment

- General outpatient consultations

Always refer to your insurer’s policy wording to understand the exact benefits and exclusions.

💰 Will Making a Claim Increase My Insurance Premium?

This is another question we hear frequently.

The short answer:

Not necessarily.

Making a claim does not automatically mean your premium will increase next year.

Instead, insurers generally review several factors during policy renewal, including:

📊 1. Claims Experience

The overall claims made by your company compared to the premiums paid is one of the biggest factors.

For example:

- Small or occasional claims may have little or no impact.

- Multiple large hospitalisation claims over a policy year may result in higher renewal premiums.

📈 2. Overall Company Claims History

Insurers look at the company’s overall claims record—not just a single worker.

A company with consistently high medical claims over several years is more likely to experience premium adjustments.

🏗️ 3. Industry Risk

Premiums may also depend on the type of work performed.

Higher-risk industries such as:

- Construction

- Marine

- Manufacturing

generally experience more workplace injuries and medical claims than office-based businesses.

💹 4. Medical Inflation

Even companies with no claims may experience premium increases because hospital treatment costs continue to rise in Singapore.

Should Employers Avoid Making Claims?

Not at all.

Insurance exists to protect employers against significant medical expenses.

If a worker requires hospitalization or surgery, employers should make legitimate claims instead of delaying treatment due to concerns about future premiums.

The better approach is to:

✔ Promote workplace safety

✔ Encourage early medical treatment

✔ Reduce workplace accidents

✔ Monitor recurring health issues among workers

These measures help improve worker wellbeing while also keeping long-term insurance costs under control.

Final Thoughts

Foreign Worker Medical Insurance is more than just a regulatory requirement—it is an important safeguard for both employers and migrant workers.

Understanding what FWMI covers, what it excludes, and how claims are assessed enables employers to make informed decisions, avoid unnecessary misunderstandings, and ensure workers receive timely medical care when it matters most.

Remember, not every doctor visit is covered, and making a genuine hospitalization claim does not automatically lead to a higher premium. Good workplace safety practices and responsible claims management remain the best way to keep both workers protected and insurance costs sustainable.

Disclaimer: This article provides a general overview of Foreign Worker Medical Insurance (FWMI) in Singapore. Coverage, claim limits, exclusions, renewal terms, and premium assessments vary between insurers and individual policy plans. Employers and workers should always refer to their specific insurance policy or consult their insurer or insurance advisor for accurate advice applicable to their circumstances.